INSOLVENCY DURING COVID-19 PERIOD

The French Parliament has by virtue of an emergency law dated 23 March 2020 empowered the French Government to take all necessary measures in order to cope with the economic, financial and social consequences of Covid-19 spread.

The Government enacted a first batch of 25 ordinances, two of which directly impact the French legal insolvency regime.

The ordinance n° 2020-306 dated 25 March 2020 related to suspension of time lapsing during the health emergency period dealing mainly with administrative and judicial time periods but also certain contractual delays and impacting pending payments suspension filing as well as creditors’ statement of claims filing.

The ordinance n° 2020-341 dated 27 March 2020 worth adaptations to insolvency rules aiming in particular at:

- the suspension of insolvency filing obligation binding on companies and their managers;

- preserving the availability of pre-insolvency proceedings even if the company becomes insolvent; and

- facilitating the formalities for filing for insolvency or for a statement of claims.

The designated purpose of such reforms consists in avoiding bankruptcies while allowing companies with difficulties to face the crisis with available tools.

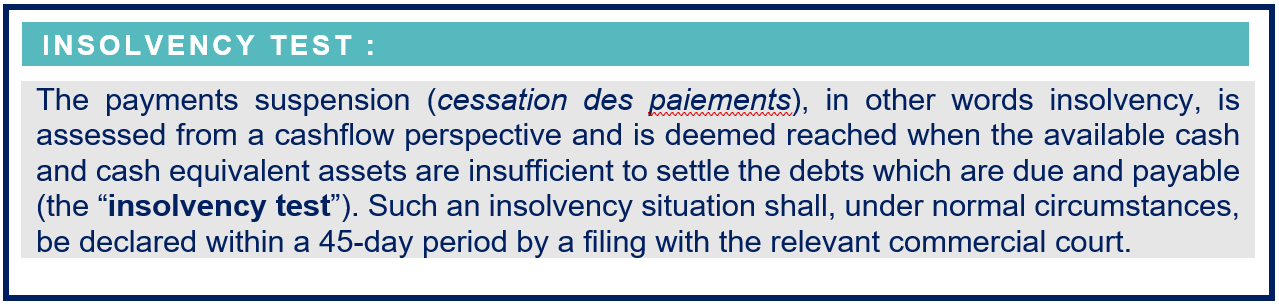

- 1.1 Principe of crystallisation of the insolvency test as at 12 March 2020

Pursuant to article I-1° of the 27 March 2020 ordinance, if, as at 12 March 2020, a company does not meet the insolvency test, it may benefit from a period of leniency.

Such a leniency period extends from 12 March (included) to 24 August 2020 (currently), which date corresponds to the expiry of the health emergency period (pending until 23 May) increased by 3 months (the ”Protected Period”).

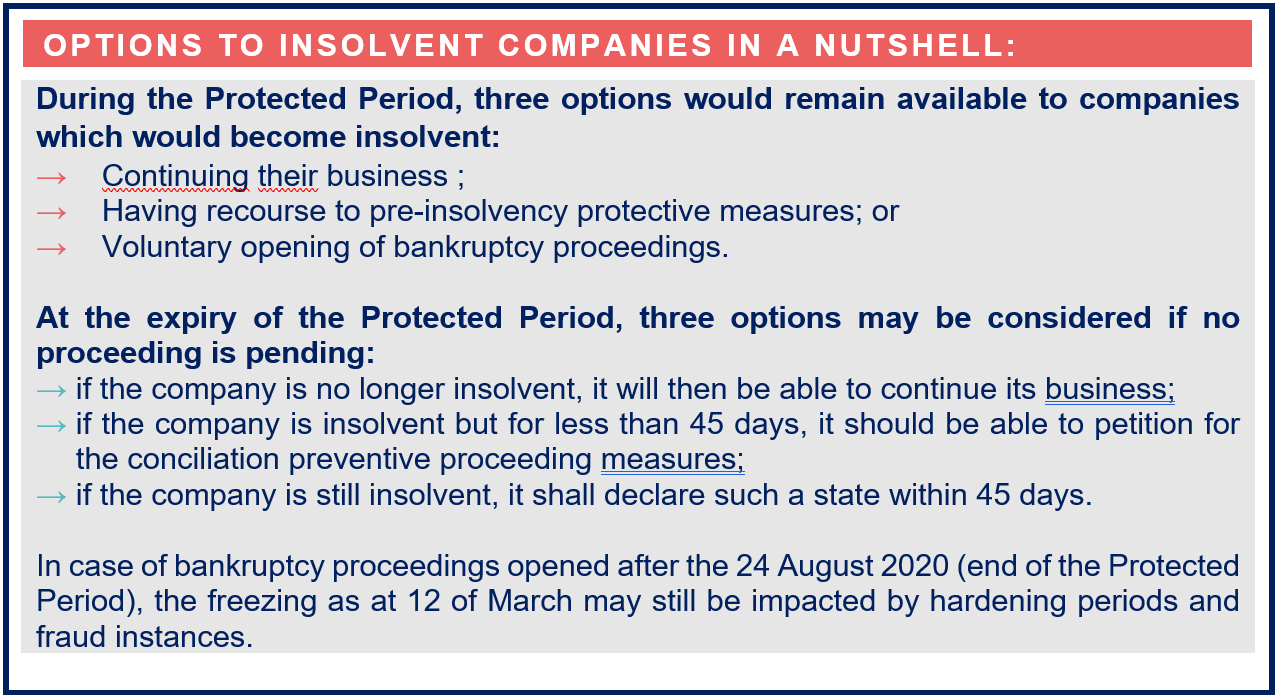

During the Protected Period, the company may, even if it becomes insolvent:

- Continue its business in the ordinary course; or

- Petition for preventive restructuring measures (ad hoc mandate, conciliation, safegard).

As a consequence, its manager(s) may not expose their liability for late insolvency filing.

At the expiry of the Protected Period:

- if the company is no longer insolvent, which means that the Protected Period will have enabled to recover, it will then be able to continue its business;

- if the company is insolvent but for less than 45 days: it should be able to petition for the conciliation preventive proceeding measures; or if the company is still insolvent: it shall declare such an insolvency within 45 days[1].

- 1.2 – Exceptions to the insolvency test freezing as at 12 March 2020

Article I-1° of the 27 March 2020 ordinance expressly provides for exceptions to the insolvency test freezing as at 12 March 2020, as follows:

- Those pertaining to the insolvent company: maintaining during the Protected Period of the option to request the opening of bankruptcy proceedings (administrative receivership – redressement judiciaire – or judicial winding-up): such option though is only open to the benefit of insolvent companies, to the exclusion of their creditors.

- Those pertaining to courts: a judicial carry back of the payments suspension date is possible under the following scenarios:

-

- Hardening period by the application of the provisions of indents 2°, 3° and 4° of article L. 631-8 of the French commercial code: the court may carry back the payments suspension date to a date prior to the judgement opening the bankruptcy proceedings. Thus, the payments suspension date could be carried back to a date that would be prior to 12 March 2020, i.e. the beginning of the Protected Period.

-

- Incase of fraud, possibility to fix a date of payments suspension that is posterior: this exception is not crystal clear but it could be construed, in our view, as allowing the judge to postpone, in case of fraud and in the instance of a later insolvency filing beyond the 12 March 2020, to fix the payments suspension date during the Protected Period, it being at a date which is posterior to the 12 March.

- Impossibility to file for insolvency of the debtor: generally, the bankruptcy proceedings can also be initiated by creditors. However, creditors are prevented from doing so during the Protected Period.

- Arrangements for filing declarations of claims:

-

- The ordinance dated 25 March 2020 applies to the declaration of claims. As a consequence, the filing, if it should take place within a period expiring between 12 March and 24 June 2020 (that is to say at the expiry of the health emergency period increased by one month), may be made until the expiry of a new period of two months running from 24 June.

Indeed, the suspension of the time limits has been provided for a shorter duration than the Protected Period, the latter being applicable for the insolvency test but also for the possible adaptations of the time limits relating to ongoing proceedings.

-

- As it stands, it seems that the ordinances have not considered the claims that should be filed by foreign companies, which are normally granted with a four-month period to file their claims. Therefore, to be on the safe side, it would be recommended to file the declaration of claims at the latest within two months as from 24 August.

“Middle East – A Region in Motion” – Insight from the Middle East Desk: MENA Legal & Market Overview, Second Semester 2025

The Middle East continues to transform at an unprecedented pace. With bold regulatory reforms, strategic investments in energy, transport, and technology, and a strong drive to diversify Gulf economies, the region remains a key player on the international stage. Discover our MENA Legal & Market Overview – Second Semester 2025, featuring insights from Joséphine Hage […]

Newsletter – Investing in France : Managing a French Company as a Foreign Executive: Visa Requirements Explained

France stands out as a prime destination for Middle Eastern investors, combining a dynamic economy, an innovation-driven ecosystem, and dedicated support measures aligned with the Gulf countries’ Vision 2030. At the same time, setting up or expanding in France brings practical challenges for business leaders, from residency and visa requirements to choosing the right legal […]

Middle East Desk | CORPORATE – M&A – PRIVATE EQUITY | ENERGY AND NATURAL RESOURCES LAW

Free Zones: a Gateway to the Middle East

The GCC has become a global trade and investment hub, with innovation-driven free zones offering vast opportunities for investors—while requiring foresight and legal expertise. To view the Newsletter, please download it using the button at the top right.

Middle East Desk | CORPORATE – M&A – PRIVATE EQUITY | ENERGY AND NATURAL RESOURCES LAW

Legal Alert – Russian Counter-Measures

Recently the Russian competent authorities have adopted new counter measures. In particular, such measures concern trade regulation, conduct of business, as well as the activities of the Government Commission and others. To find out more, download the Newsletter or click here. For more information on sanctions and Russian counter measures, please refer to our previous “Legal Alerts“.

Desk Russia, Central Asia and Caucasus

Sanctions Against Russia. Recent Developments

On 23 February 2024 European Union and the United States introduced a new round of sanctions targeting Russia. The 13th package of European sanctions provides for new individual sanctions, sectoral sanctions, export restrictions. Additionally, EU added the United Kingdom to the list of partner countries for the iron and steel import restrictions. American sanctions include […]

Desk Russia, Central Asia and Caucasus

Newsflash – Corporate – Venture Capital – French government announcements to support Innovative Startup Companies (JEI)

For the occasion of the French Tech’s 10th anniversary, new measures stemming from the report of Parliament Member Paul Midy (for which Jeantet had been consulted) have been announced. These measures, which aim at supporting the French startup ecosystem, should be included in the next Finance Act for 2024. ► Doubling of companies eligible to […]

| CORPORATE – M&A – PRIVATE EQUITY

Russian Counter Measures. Recent Developments

On 23 August, the Russian Ministry of Finance partially lifted a ban for the payment of dividends to foreign shareholders in case such shareholders have invested in the Russian economy. On 8 August, the Russian President suspended certain provisions of double tax treaties. Suspended provisions include tax regime for dividends, real estate, business profit, etc […]

Desk Russia, Central Asia and Caucasus

Sanctions Against Russia. Recent Developments

On 23 June 2023, the EU introduced 11th package of sanctions. It primarily focuses on measures that would prevent circumvention of sanctions. It also includes new import and export restrictions and individual designations. Switzerland has joined European Union in sanctions targeting entities and individuals and may join other sanctions within the 11th package in August. […]

Desk Russia, Central Asia and Caucasus

Newsletter – Tax law

Read the Jeantet Newsletter dedicated to Tax Law, covering issues related to : Transactional taxation Group taxation International Taxation Taxation of LBO transactions Non-profit organizations For more information, please download the Newsletter.

Paris | TAX

Russian Counter Measures

On 25 April 2023 Russian President issued a decree establishing cases authorizing him to introduce the regime of external management of certain assets owned by foreign residents. Namely, under the decree, the President may establish the regime of external management, if Russia, or its entities and individuals become deprived or risk of being deprived of […]

Desk Russia, Central Asia and Caucasus

Russian counter measures and measures aimed at business support. Recent developments

Special regime for transactions involving securities On 3 March 2023 Russian President issued Decree No. 138 establishing additional measures involving securities. Namely, the new Decree establishes a specific procedure for transactions / operations involving: shares of Russian joint-stock companies, sovereign bonds, bonds of a Russian issuer, held in collective safe custody of a Russian depository, […]

Desk Russia, Central Asia and Caucasus

Sanctions against Russia. Recent developments (2 march 2023 update)

By the end of February, the EU, US and UK announced new rounds of sanctions, all of them including restrictions targeting prominent Russian financial institutions The EU package includes individual listings of Russian entities and individuals and additional exports restrictions. The US sanctions provide for sectoral sanctions targeting Russian mining and metals sector, as well […]

Desk Russia, Central Asia and Caucasus